A friend of mine spent three years reading Rich Dad Poor Dad and nodding along to Kiyosaki's ideas about assets and cash flow. She felt inspired every time she picked it up. The problem was, she also had $22,000 in credit card debt sitting at 24% interest. She never touched it. Meanwhile, her coworker bought The Total Money Makeover on a Tuesday, followed the baby steps, and had that same category of debt gone in 14 months. Two different books. Two very different outcomes. The question was never which book is better in the abstract. It was which one was right for where each person was sitting.

Rich Dad Poor Dad by Robert Kiyosaki is one of the bestselling personal finance books ever printed, with more than 40 million copies sold. The Total Money Makeover by Dave Ramsey has its own devoted following, with over 22,000 reviews on Amazon averaging 4.7 stars. Both are genuinely worth reading. But they are teaching different things, written for different problems, and they will pull you in different directions if you try to follow both at once. I want to help you figure out which one belongs in your hands right now.

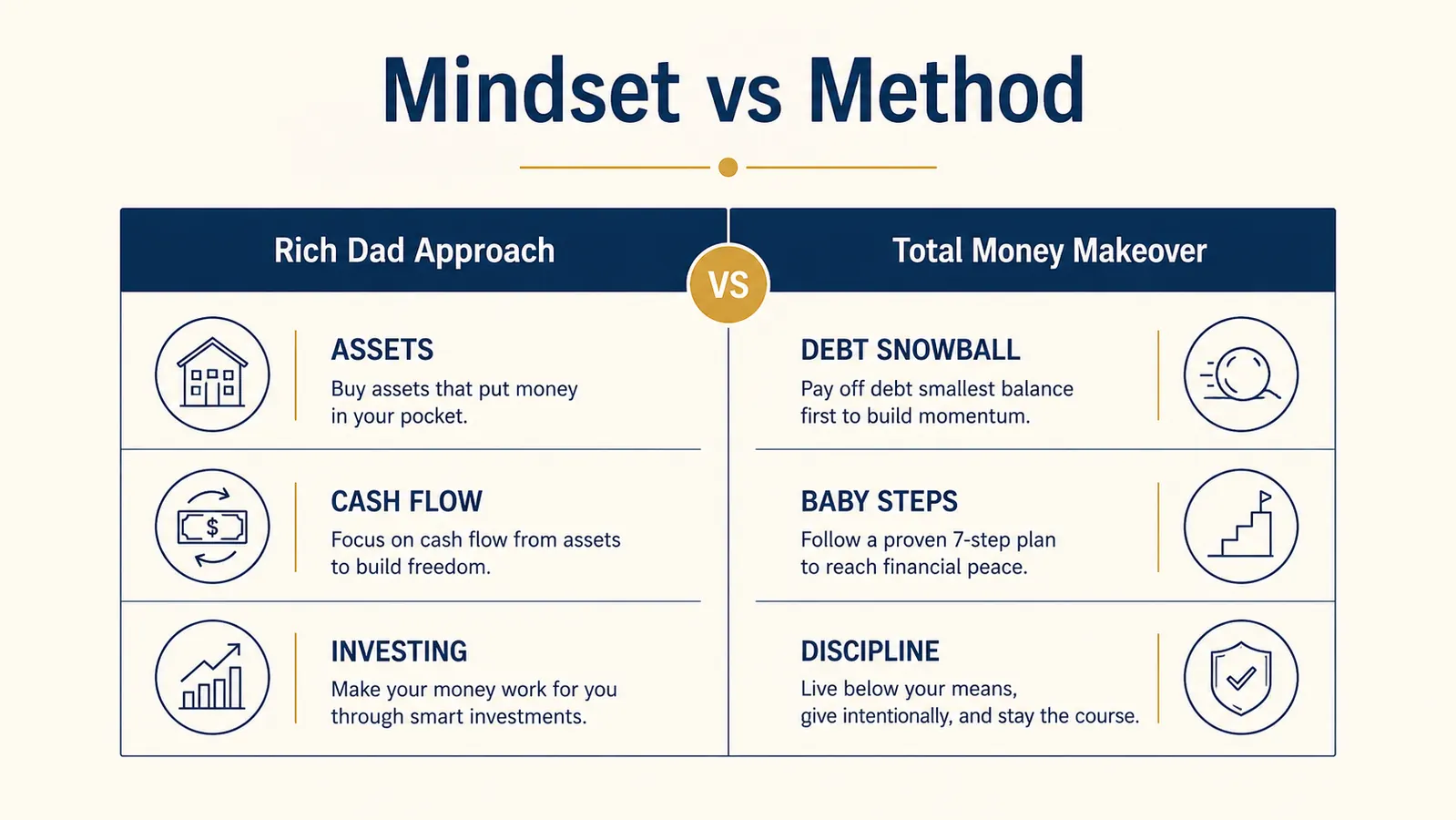

| Rich Dad Poor Dad | Total Money Makeover | |

|---|---|---|

| Core Philosophy | Build income-producing assets; stop trading time for money | Eliminate all debt using the baby steps; live on less than you earn |

| Primary Focus | Financial mindset shift and long-term wealth building | Practical, numbered action plan for debt payoff and savings |

| Debt Treatment | Some debt (used to buy assets) can be acceptable | All consumer debt must go before you invest; debt snowball method |

| Best For | Readers stuck in an employee mindset who have never thought about assets or passive income | Readers drowning in credit cards, car loans, or student debt who need a clear step-by-step plan |

| Investment Guidance | Real estate, small business, paper assets; broad concepts, limited specifics | Mutual funds in tax-advantaged accounts after Baby Step 3; specific and prescriptive |

| Writing Style | Parable-style storytelling; conversational and motivational | Direct, authoritative, tough-love instruction |

| Criticism | Vague on specifics; some advice requires significant capital to act on | No tolerance for nuance; investing advice oversimplifies for high earners |

| Amazon Reviews | 4.7 stars, 107,677+ ratings | 4.7 stars, 22,306+ ratings |

Where Rich Dad Poor Dad Wins

Rich Dad Poor Dad wins on mindset. That sounds soft, but it matters more than people give it credit for. Most of us grew up with the same financial script: go to school, get a job, earn a salary, pay bills, maybe save a little, retire someday. Kiyosaki is the first book most people ever encounter that directly challenges that script. He draws a sharp distinction between assets (things that put money in your pocket) and liabilities (things that take money out). That one idea, simple as it sounds on the page, genuinely shifts the way a lot of readers look at their income, their spending, and their time.

I read Rich Dad Poor Dad for the first time when I was 27, earning a decent salary and spending almost all of it. I had never once asked myself whether the things I was buying made me richer or poorer over time. After that book, I started asking. That is not nothing. The mindset shift is real, and for readers who have never been exposed to the concept of building assets outside of a 9-to-5 salary, this book is genuinely eye-opening. It also has the longest staying power of any finance book I have come across. People who read it 20 years ago still reference the core ideas.

Where The Total Money Makeover Wins

The Total Money Makeover wins on execution. If you have debt, Ramsey's system is the most actionable, most clearly laid out plan you will find between two covers. The seven baby steps are numbered, sequenced, and explained with almost no room for ambiguity. Baby Step 1: save a $1,000 starter emergency fund. Baby Step 2: list all your debts smallest to largest, pay minimum payments on everything except the smallest, then throw every extra dollar at it until it is gone. Repeat. The debt snowball is psychologically smart, and for most readers with real consumer debt, it works.

The Total Money Makeover is also more honest about the role of behavior. Ramsey understands that most personal finance problems are not really math problems. They are behavior problems. Knowing that you should save more does not make you save more. Having a clear script to follow, with specific dollar targets and a sequence that produces small wins early, does. That is what the baby steps deliver. For the reader who has been inspired by many books and taken action on none of them, Ramsey's structured approach is exactly what is missing.

Still carrying debt while Kiyosaki's asset ideas sit on hold? Read Rich Dad Poor Dad first to shift your thinking, then decide your next move.

Rich Dad Poor Dad has over 107,000 Amazon reviews and a 4.7-star rating. It is one of the most-read personal finance books in history for a reason. Check today's price and see what current buyers are saying.

Amazon Check Today's Price on Amazon →Rich Dad teaches you what to think about money. Total Money Makeover teaches you what to do with it. The catch is that what to do only sticks once your thinking changes.

The Real Tension Between These Two Books

Here is the honest tension: Kiyosaki and Ramsey disagree on debt in a fundamental way. Ramsey says all consumer debt is bad, period. He wants you to pay it off before you invest a dollar. Kiyosaki draws a line between bad debt (credit cards, car loans) and what he calls good debt (borrowing to buy an income-producing asset like a rental property). For people with no consumer debt and some capital to work with, the distinction makes sense. For someone carrying $15,000 in credit cards at 22%, trying to figure out how to buy assets using Kiyosaki's framework while paying hundreds in monthly interest is a recipe for spinning your wheels.

I have seen both play out. People who read only Rich Dad Poor Dad sometimes stay stuck in inspiration mode for years. They understand the concept of passive income but never get traction because they are bleeding money to debt service every month. People who read only The Total Money Makeover sometimes pay off debt successfully and then get too conservative, keeping everything in savings accounts long after the debt is gone because they are still in debt-elimination mode. Neither book alone gives you the complete picture.

Who Should Buy Which

Start with Rich Dad Poor Dad if you have never seriously questioned the earn-and-spend cycle, if you feel like you are working harder every year but not getting ahead, or if no one in your life ever talked about investing, assets, or building something outside of a paycheck. The mindset shift this book creates is the foundation everything else builds on. You cannot follow a wealth-building plan if you fundamentally believe that working harder at your job is the only way forward. Rich Dad breaks that belief, and it does it in a way that sticks.

Start with The Total Money Makeover if you have active consumer debt and you need a plan right now. Student loans, car payments, credit cards: if any of those are on your statement, Ramsey's baby steps are your clearest path to the starting line that Kiyosaki assumes you are already standing on. Get the debt gone, build the emergency fund, and then the concepts in Rich Dad become much more applicable to your actual situation.

If you are somewhere in the middle, here is what I would do. Read Rich Dad Poor Dad first, because the mindset piece is genuinely harder to acquire than the tactical steps. Then read The Total Money Makeover to get a concrete action plan that reflects where you are now financially. The two books are not enemies. They are addressing different layers of the same problem.

A Word on What Each Book Is Not

Rich Dad Poor Dad is not a step-by-step instruction manual. If you go in hoping for a numbered list of exactly what to do this week, you will leave frustrated. Kiyosaki writes in parables and broad principles. The details are on you to figure out. That is a real limitation, and the critics who knock the book for being vague are not wrong. It plants seeds. It does not build the garden for you.

The Total Money Makeover is not a wealth-building book in the Kiyosaki sense. It will help you stop the bleeding and build a solid foundation. But if your goal is to own income-producing assets or build a business, Ramsey gets prescriptive in ways that do not always fit. He is firmly pro-mutual-fund and fairly skeptical of real estate investing outside of a paid-off primary home. That is a conservative stance that works well for people prone to taking on too much risk, but it can feel limiting once you have the basics handled.

Both books are worth the investment of a few hours. Both have flaws that are worth knowing about before you read them. And both have helped real people in real ways, which is why they are still being printed and read decades after they were first published.

If you are going to read one book to shift how you think about money, Rich Dad Poor Dad is still the best starting point.

Over 107,000 readers have reviewed it on Amazon with a 4.7-star average. It has been in print for decades for a reason. Check today's price and see if it is the right fit for where you are right now.

Amazon Check Today's Price on Amazon →