I want to give you a straight answer up front: if you pay for most things in cash or struggle with overspending when money feels invisible, the SKYDUE Budget Binder is the better tool. If you use cards for everything and already track purchases without a second thought, YNAB is worth a look. The rest of this comparison explains the reasoning, so you can make the call that actually fits your life and your habits, not someone else's. Neither system is magic. The one that gets used consistently wins, and that depends almost entirely on how your brain responds to spending feedback.

Both tools are genuinely popular. The SKYDUE Budget Binder has nearly 20,000 Amazon reviews at a 4.7-star average. YNAB has a loyal following and tends to show up on personal finance forums with passionate advocates. But popular does not mean right for you. These two tools work through completely different psychological mechanisms, and choosing the wrong one for your spending habits is like wearing the wrong glasses: everything stays blurry no matter how hard you squint. Let me break down exactly where each one earns its place.

| SKYDUE Budget Binder | YNAB App | |

|---|---|---|

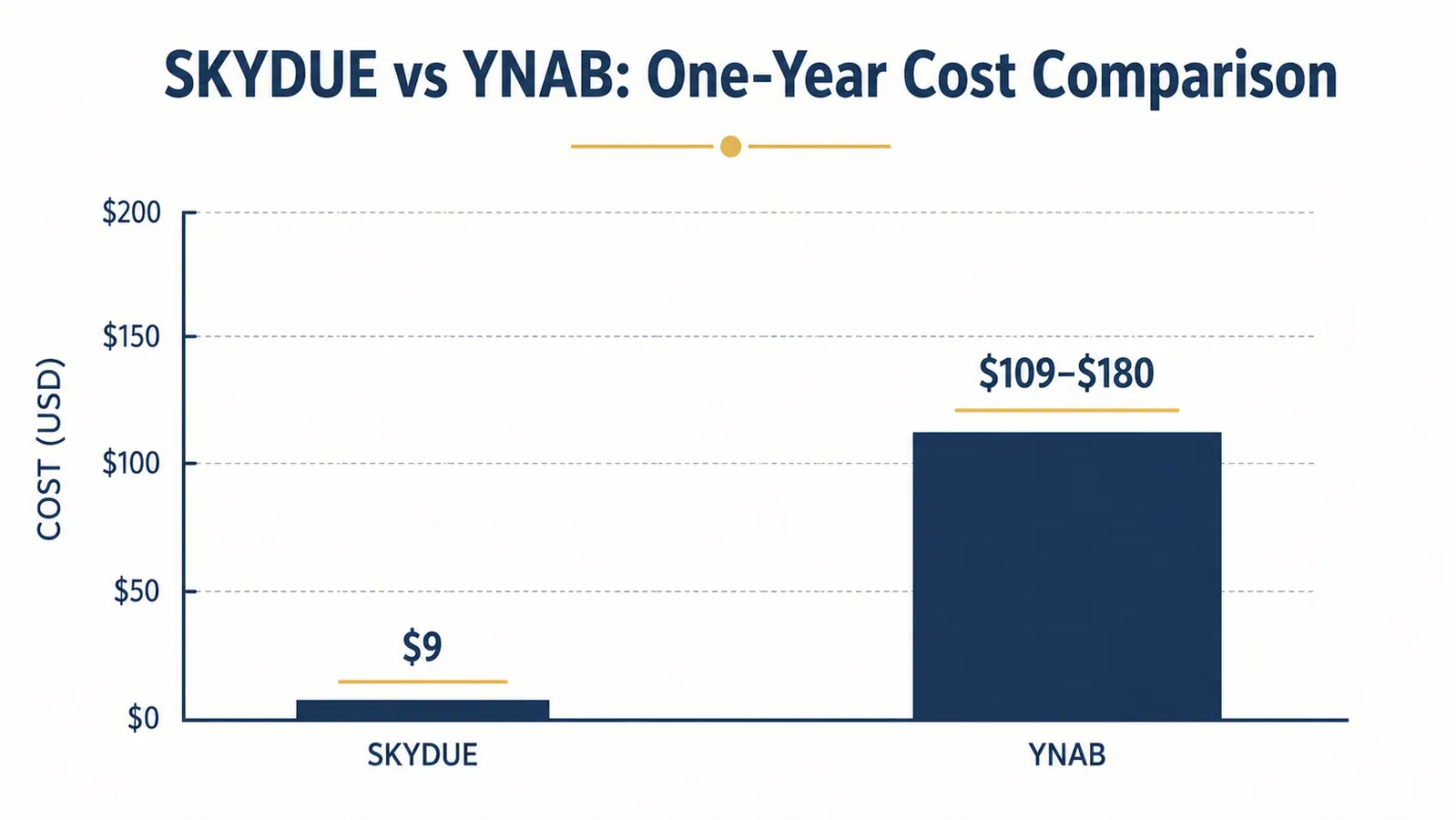

| Price | Around $9 one-time purchase, no subscription required | $14.99 per month or $109 per year subscription |

| One-Year Total Cost | About $9 total | About $109 to $180 depending on billing cycle |

| Format | Physical binder with 12 zipper cash envelopes and expense tracking sheets | Smartphone app and web dashboard with bank sync and automatic transaction import |

| Best For | Cash spenders, visual learners, and anyone who overspends when using cards | Digital-first users who prefer bank sync and automatic transaction categorization |

| Setup Time | About 30 minutes to label envelopes and fill them on payday | About 60 to 90 minutes to link accounts, import history, and learn the interface |

| Learning Curve | Very low. You put cash in, you spend cash out, the envelope balance is your answer | Moderate. YNAB uses a unique budgeting philosophy that takes several pay periods to internalize |

| Offline Access | Always available with no internet or phone required | Requires a phone and internet connection; limited offline functionality in the app |

| Spending Friction | High by design. Physically handing over cash makes every purchase feel real and deliberate | Low by design. You swipe your card as usual and record or import the transaction afterward |

| Included Items | 12 zipper envelopes, expense budget sheets, pen loop, and a calculator pocket | App access only; no physical materials included |

Where the SKYDUE Budget Binder Wins

The biggest win for the SKYDUE binder is what behavioral researchers call the 'pain of paying.' When you physically hand someone a twenty-dollar bill, your brain registers the loss in a way that tapping a card or clicking 'buy' never triggers. That friction is not a bug in the system. It is the whole point. My neighbor Terri, a school cafeteria worker supporting two kids on a single income, tried three different budget apps over two years and each one fizzled out within a few weeks. She told me the problem was never knowing her budget. She knew. The problem was not feeling it. She started using a cash envelope binder in January and by April she had her first $500 buffer set aside. Nothing about her income changed. Her relationship with spending changed because the money became something she could see and touch, not just a number on a screen that refreshed overnight.

The SKYDUE binder is also the clear winner on long-term cost. You pay once and that is it. At the current price on Amazon, most people break even compared to YNAB's monthly fee in the first two weeks of using it. Over a full year, the savings are significant, and that money can go straight into the envelopes themselves. The binder also comes with expense tracking sheets, so you can log what you spend in each category without any app, subscription, or internet connection. For someone who works overnight shifts, lives somewhere with spotty service, or simply does not want to hand over bank login credentials to a third-party app, that independence matters. It works the same way on day one as it does on day three hundred and sixty-five.

One more thing the binder does well: it forces a money conversation with yourself. When you sit down on payday to fill your envelopes, you are making a decision about every dollar before it gets spent. That weekly or biweekly ritual is where the real budget work happens. Most people who use digital apps skip that ritual because the app does the categorizing in the background. The consequence is that you end up reviewing spending after the fact instead of deciding ahead of time. With a binder, you set your intentions first. That forward-looking posture is what makes the cash envelope method so effective for people who have spent years being reactive with money rather than proactive.

Where YNAB Wins

YNAB is genuinely well-designed software for people who live a card-based financial life. If you pay rent, utilities, and groceries with a debit or credit card and rarely carry cash, pulling out envelopes creates its own logistical headaches. You still have to withdraw cash from an ATM on payday, keep it organized at home, and remember to bring the right envelope when you head out. If you forget the grocery envelope and you are already at the store, you either drive home or swipe the card and try to sort it out later. YNAB removes all of that friction by connecting directly to your bank and credit card accounts and automatically importing what you spend. For a freelancer running all expenses through one business card, or someone who does most shopping online, that kind of automation actually makes sense.

YNAB also has a deeper reporting layer than anything you can replicate with a paper expense sheet. You can look back at three months of spending by category, spot a pattern like restaurant spending creeping up 40 percent in February, and adjust your forward budget accordingly. The binder's expense sheets give you a running record within each envelope, but historical analysis requires you to do the math yourself or save old sheets. If you genuinely enjoy diving into numbers and want data to back every budget decision, YNAB provides that depth. The tradeoffs are the monthly cost and the real risk of spending more time tinkering with the system than actually changing your spending habits, which is a trap more users fall into than YNAB's marketing acknowledges.

If you keep running out of money before the month ends, cash envelopes can fix that in one payday cycle.

The SKYDUE Budget Binder comes with 12 labeled zipper envelopes, expense tracking sheets, and a pen loop. Nearly 20,000 buyers have reviewed it at 4.7 stars. Most people are up and running in under 30 minutes, with no subscription and no app required.

Amazon Check Today's Price on Amazon →Who Should Buy Which

Here is the simplest way I know to decide. Think about the last time you overspent a budget category. Was it because you did not know the money was gone, or because you knew and spent it anyway? If you did not know, either tool can help because either one will make you more aware of where the money goes. But if you knew and spent anyway, that is a habits and impulse-control problem, not an information problem. For that pattern, physical cash is the better teacher. Pulling a twenty from a grocery envelope and watching it leave your hand creates a moment of real hesitation that no push notification from any app has consistently replicated for most people who struggle with overspending.

If you are living paycheck to paycheck, working toward your first savings cushion, or trying to stop the cycle of overdraft fees and late payments, start with the cash envelope binder. The upfront cost is low, the learning curve is minimal, and the psychological effect kicks in the very first time you fill your envelopes. You do not need to connect a bank account, learn new software, or pay a subscription to get started. You need cash, a binder, and a list of your monthly spending categories. That is the whole setup.

If you are already out of the paycheck-to-paycheck cycle, you use cards for everything, and you want detailed spending analytics to optimize a stable financial life, YNAB is built for exactly that kind of user. It is not really a beginner's tool despite its beginner-friendly marketing language. It rewards people who are already somewhat organized and want to go deeper into the numbers. If that is where you are right now, the monthly subscription might genuinely pay for itself through one or two spending decisions you would have otherwise made blindly. But be honest with yourself about which stage of the journey you are actually in before committing to a recurring charge.

Physical cash creates a moment of hesitation that no app notification has consistently replicated. That hesitation is the budget working.

One more option worth knowing about: you do not have to pick just one system forever. Several readers I have talked with use the SKYDUE binder for their three or four biggest variable spending categories, specifically groceries, eating out, and household miscellaneous, and handle fixed bills by autopay without thinking about them at all. That hybrid approach costs almost nothing and attacks the categories most likely to blow a budget month after month. You get the tactile accountability where you need it most, without the hassle of managing cash for every single purchase. It is a practical middle path and, honestly, the one I would recommend to most people who are just starting to take budgeting seriously.

For a deeper look at how the SKYDUE binder holds up over six months of daily use, including what I struggled with in the beginning and what surprised me most by month four, check out the full long-term review linked below. And if you are ready to get started today, the step-by-step guide to setting up a cash envelope budget with the SKYDUE binder walks you through your first payday from start to finish, including which spending categories to create and how much cash to put in each one based on your income and fixed expenses.

The SKYDUE binder costs less than a dinner out and has helped nearly 20,000 people take control of their spending.

It comes with 12 zipper cash envelopes, expense budget sheets, a pen loop, and a built-in calculator pocket. No subscription required, no login, no app updates needed. Just a system that makes your money visible and your spending decisions deliberate from the first payday you use it.

Amazon Check Today's Price on Amazon →