Let me tell you what nobody said to me before I bought this book. I was 31, working as a project coordinator for a mid-size construction company, making decent money for the first time in my adult life. A colleague at a team lunch mentioned Rich Dad Poor Dad the way people mention the Bible, like everyone has already read it and you are slightly embarrassing yourself by admitting you have not. So I ordered a copy that same evening. I expected a roadmap. I wanted to know what to do with the $400 a month I had finally started putting away. What I got instead was a philosophy without instructions, and I sat with a mix of genuine inspiration and quiet frustration for weeks afterward. That tension is exactly what this review is about.

Rich Dad Poor Dad by Robert T. Kiyosaki has over 107,000 reviews on Amazon and a 4.7-star average. It has been in print since 1997 and has sold more than 40 million copies worldwide. It has also been the subject of serious criticism from financial journalists, certified planners, and former fans who felt misled. My goal here is not to pile on and not to defend the book uncritically. My goal is to give you an honest accounting of what you will and will not get from reading it, so you can decide whether it belongs on your list.

The Quick Verdict

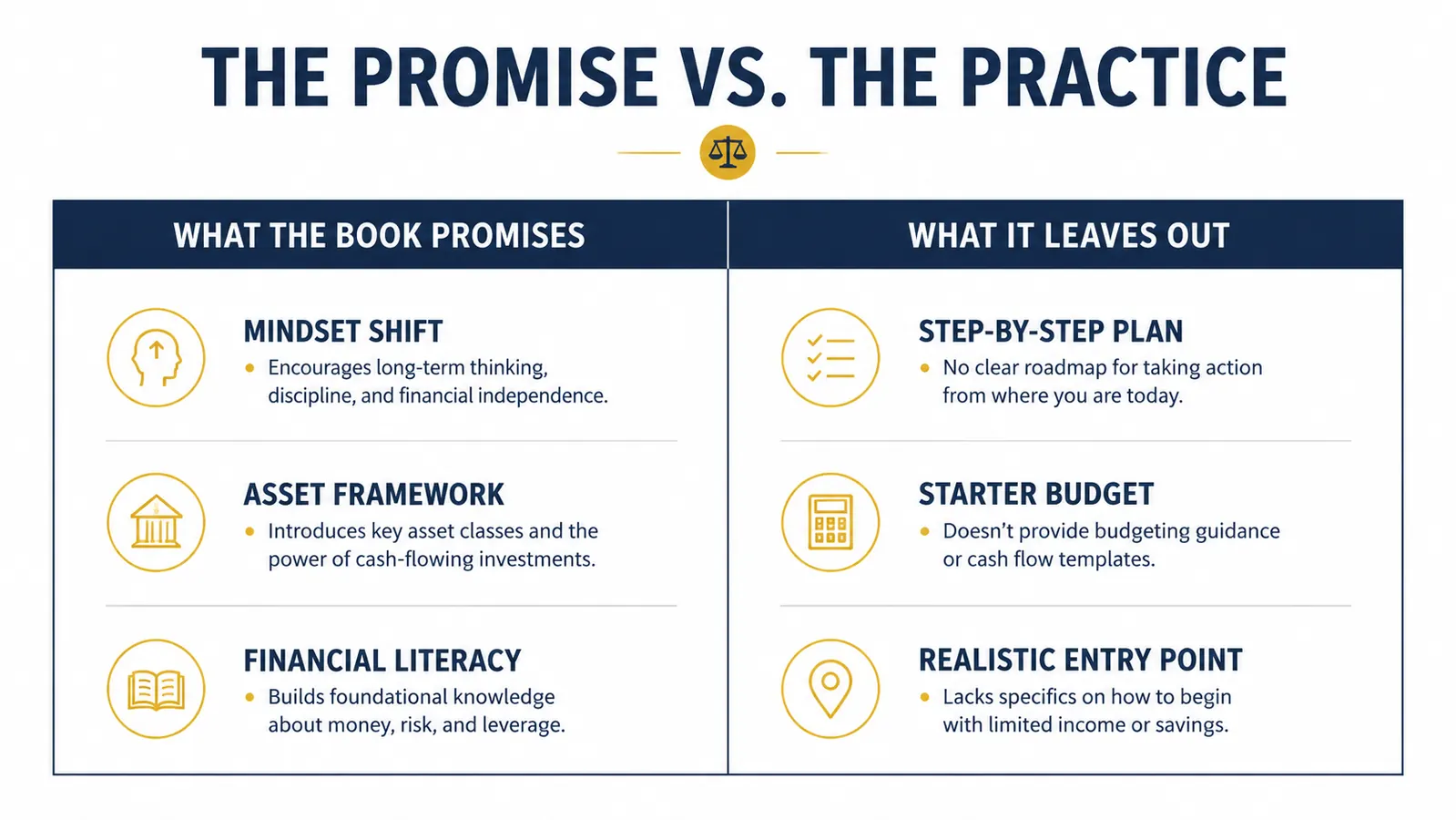

A valuable mindset primer that will reframe how you think about money, but it leaves a real gap between the ideas it sells and the action steps it refuses to give you.

Amazon Check Today's Price →Still trading hours for dollars and wondering why nothing is building? The book names why.

Rich Dad Poor Dad will not give you a budget template or a step-by-step savings plan. What it gives you is a framework for why those tactics often fail without a deeper shift in thinking first. It is available in paperback, Kindle, and audio. Check current pricing on Amazon.

Amazon Check Today's Price on Amazon →How I Read It and What Actually Happened

I read the book in about three evenings. It moves fast. Kiyosaki writes in a conversational style, and the story format, drawn from his childhood relationship with two father figures, pulls you along even when the financial concepts get repetitive. By the time I finished, I had underlined probably thirty passages and filled a full page of my notebook with words like "cash flow," "passive income," and "acquire assets." I felt like something had clicked.

Then I sat down the next morning to turn that click into a concrete plan, and I ran into the wall that a lot of readers hit and do not talk about publicly. There was no plan. The book teaches you that you should buy assets. It does not tell you how to evaluate a rental property, how to start a side business from a salaried job, how much cash you need before taking on investment risk, or what to do if you have no savings and a student loan payment every month. I spent the following two weeks reading message boards trying to reverse-engineer what the book was actually telling me to do. That is not a criticism of the philosophy. It is a factual description of the experience the book delivers.

What eventually happened is this: I paired the mindset shift from this book with a separate, more tactical resource and started putting $400 a month into a low-cost index fund through my brokerage account. Within eight months, I had moved that to $600 a month. That discipline did not come from this book, but the reason I stopped spending that money on things that would depreciate did. The book changed my framing. Another book gave me the plan. Both were necessary.

The Rich Dad Debate: What You Should Know Before You Trust the Source

There is something that deserves to be said plainly because most reviews either ignore it or use it to dismiss the book entirely. The "rich dad" at the center of this story, Kiyosaki's friend's father who mentored him on money, has never been publicly identified. When journalists have pressed Kiyosaki on this, the answers have been inconsistent. He has suggested at various times that rich dad was a composite character, a real person who wished to remain anonymous, and a true mentor. John T. Reed, a real estate investment educator who wrote a detailed critique of the book, concluded that the events described are implausible as literal biography.

What does that mean for you as a reader? It means the book is better understood as a financial parable than as memoir. The lessons it teaches, particularly the distinction between assets and liabilities, are real and useful regardless of whether rich dad existed. But the framing of the book asks you to trust a specific relationship and a specific story as the origin of these ideas, and if that story is more constructed than biographical, it matters for how you weigh the advice. Know that going in. Treat the ideas on their own merits rather than because a mentor figure endorsed them.

Kiyosaki's personal financial record also deserves mention, not to pile on, but because readers evaluating advice should know the adviser's track record. His company Rich Global LLC filed for Chapter 7 bankruptcy in 2012 following a legal dispute over a speaking engagement deal. He has since rebuilt and his personal net worth is often reported as substantial, built largely through book sales and seminars rather than the real estate and business investments the book describes. He has also made public calls on gold, silver, and Bitcoin that have been controversial in timing. None of this voids the mindset framework in this book. But a reader who treats Kiyosaki as an infallible financial authority, rather than an author with a useful perspective and a mixed track record, is setting themselves up for disappointment.

What the Book Gets Right That Critics Dismiss Too Quickly

The critics of this book, and there are credentialed ones, tend to fixate on what it lacks: specific investment guidance, a step-by-step plan, an accountant's precision. Those criticisms are fair. But they often cause reviewers to throw out the parts of the book that are genuinely valuable, and those parts are not small.

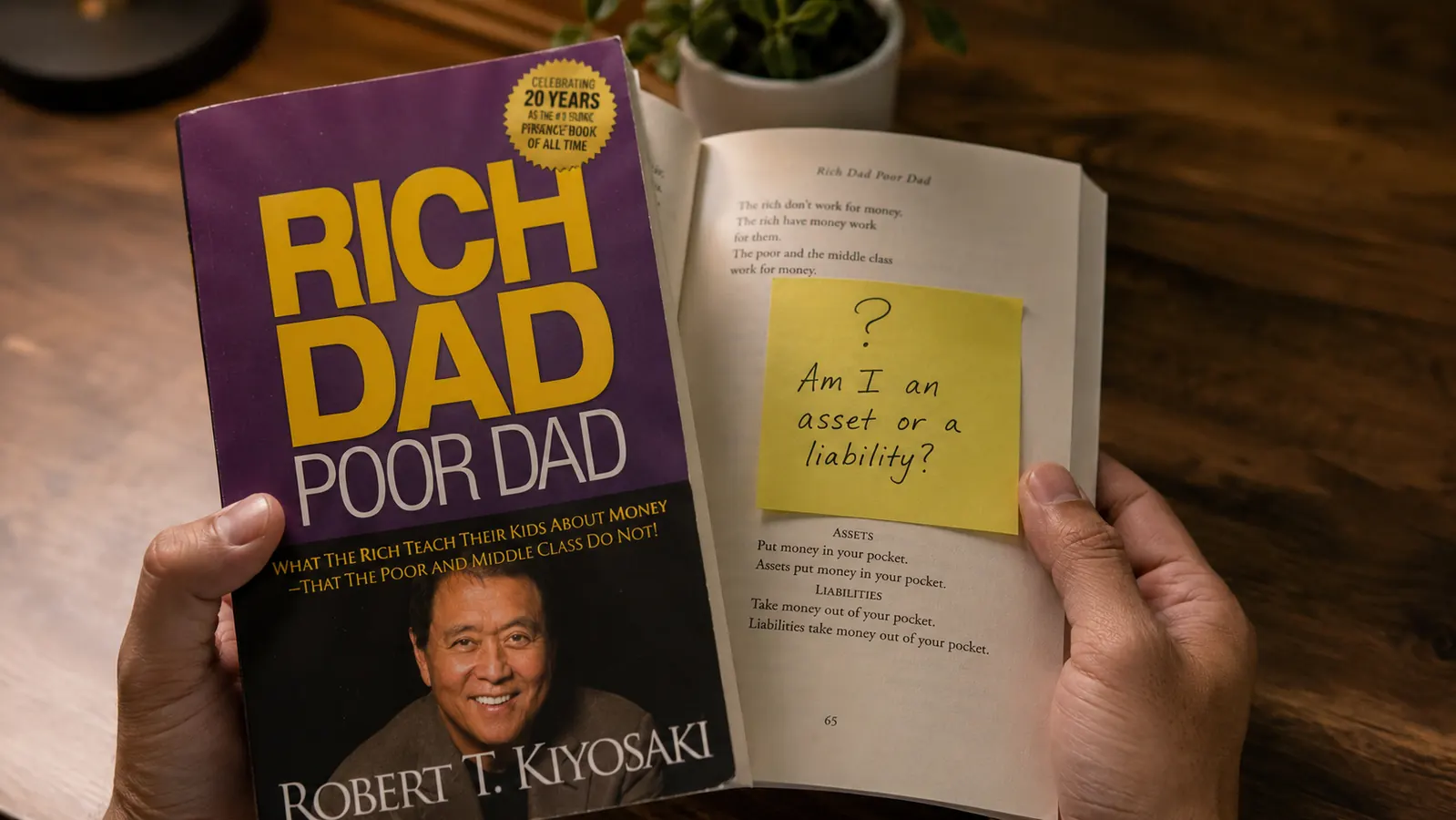

The central distinction between assets and liabilities, as Kiyosaki defines them, is not taught in schools and is not intuitively obvious. Most people grow up being told that owning a home is the goal, that a nice car is a sign of success, and that job security is the path to financial stability. Kiyosaki pushes back on all three of those assumptions in a way that is blunt and memorable. His definition, assets put money in your pocket, liabilities take money out, sounds simple, but applying it consistently changes how you look at every major financial decision. That shift is not nothing. For a reader who has never encountered this framing before, it can be the beginning of a genuinely different relationship with money.

The book is also right about financial education as a systemic gap rather than a personal failure. Kiyosaki frames poor money management not as laziness or weakness but as a predictable outcome of a system that never teaches people how money actually works. That framing is motivating rather than shaming, and it tends to open readers up to learning rather than shutting them down with guilt. That is a real contribution.

The book does not give you a plan. But it gives you a reason to want one badly enough to go find it. For a lot of readers, that is the missing piece.

Where Readers Feel Let Down and Why It Happens

The gap between the book's ambition and its specificity is where most readers hit friction, and it tends to land hardest on people who are already under financial stress. If you are carrying credit card debt, you finish this book knowing that acquiring assets is the answer, but the book offers little about how to prioritize debt payoff, what to do before you can invest, or how to build a financial foundation. The implied message can feel like: figure it out yourself, the way rich dad did.

The real estate focus compounds this. Kiyosaki's preferred asset class is rental property, which today requires substantial upfront capital, good credit, and local market knowledge. In expensive metro areas where many readers live, the entry point for the kind of real estate Kiyosaki describes is $50,000 or more in down payment. The book does not acknowledge that barrier seriously. It mentions finding deals and thinking creatively, but it does not map a path from zero savings to first investment property in a way that translates to most readers' actual situations.

The tone is worth flagging too. Kiyosaki has a way of writing about people who stay in salaried jobs as if they are making a kind of moral error. The book celebrates the self-employed and the investor while treating employment as a trap for people who lack courage or vision. If you are a nurse, a teacher, or someone who builds a meaningful career within an organization and finds satisfaction there, this book will occasionally feel like it is calling you a coward. That is not fair. It is also not reflective of how most people build financial security in the real world.

What I Liked

- The asset versus liability framework is clear, memorable, and genuinely useful for reframing spending decisions

- Positions financial ignorance as a systemic gap rather than a personal flaw, which is motivating rather than shaming

- Written in an accessible narrative style that moves fast and keeps you engaged across a weekend read

- The chapter on how taxes treat employees versus business owners is eye-opening and factually accurate

- At current pricing, it is among the lowest-cost mindset investments you can make in your financial education

Where It Falls Short

- Provides almost no actionable steps between the inspiration and the outcome it describes

- The rich dad origin story has been credibly questioned as more parable than biography, which affects trust

- Heavy focus on real estate as the primary asset class excludes or confuses readers without significant capital

- Dismissive of salaried employment in a way that does not reflect how most people actually build financial stability

- Kiyosaki's own financial history, including a corporate bankruptcy, is not mentioned and is relevant context for the reader

The Most Common Mistake Readers Make With This Book

The biggest error I have seen, and the one I almost made, is treating this book as a complete education rather than an opening chapter. People read Rich Dad Poor Dad, feel motivated, and then either burn out when they cannot find an actionable next step, or they follow Kiyosaki's specific recommendations into investment decisions they are not prepared for. Both of those outcomes are avoidable if you are clear about what the book actually is.

Think of it this way: this book is useful for answering the question of why you should think differently about money. It is not useful for answering the question of what to do tomorrow morning. If you read it looking for the second answer, you will be disappointed. If you read it as a primer that helps the second answer make more sense when you go looking elsewhere, it earns its place in your reading stack.

In my case, reading this book made the index fund literature click in a way it had not before. I had tried to read about passive investing previously and gotten lost in the mechanics without understanding why it mattered. After this book, I understood what I was building toward, and the mechanics became meaningful. That sequencing matters. Rich Dad Poor Dad is probably best read first, not last.

Who This Is For

This book works best for someone who is new to thinking about money strategically, who earns a paycheck but has no framework for what to do with it beyond paying bills and maybe saving a little, and who responds to story-driven explanations over technical ones. If you have ever thought about investing but could not answer the question of why, this book tends to supply that why in a way that sticks. It also works well for someone who has been told by a friend or mentor to read it and wants to understand what the conversation is about. That was me. I am glad I read it, reservations and all. If you want to see how the book compares to a more structured, step-by-step approach, our comparison of Rich Dad Poor Dad against Dave Ramsey's method walks through which philosophy suits which kind of reader. And if you want to go deeper on the specific lessons without re-reading the whole book, there is a breakdown of the ten money ideas from Rich Dad Poor Dad that stay useful even if you skip the real estate chapters.

Who Should Skip It

If you are in active debt trouble and need a structured payoff plan this week, skip this book for now. It will not help you on that timeline. If you are already financially literate and looking for investment strategy with real depth, this book will feel thin. If you are sensitive to the real estate focus and looking for advice that maps to your actual financial situation as a salaried professional without capital to deploy, you may finish the book more confused than when you started. And if source credibility matters to you, the questions around the rich dad story and Kiyosaki's broader track record are things you should know about before forming a strong opinion on his advice. The ideas in this book are worth considering on their own terms. The messenger has a more complicated history than the book lets on.

If you have been meaning to get serious about money but cannot explain why you have not yet, this is a good place to start.

Rich Dad Poor Dad will not give you a plan, but it will give you a reason to want one. For the price of a paperback, it shifts the question you ask before every financial decision. Read it first, then find the tactical book that fills the gap it leaves. Check current availability and pricing on Amazon.

Amazon Check Today's Price on Amazon →