I have talked with a lot of people who feel stuck. They make enough to survive but never enough to get ahead. They have tried budgeting apps, YouTube finance advice, and more than a few fresh starts on January 1st. None of it held. Then someone handed them a copy of The Total Money Makeover by Dave Ramsey, and something clicked. I have seen this happen enough times that I want to walk through exactly why the plan works, not just that it works.

The Baby Steps system Ramsey lays out in the book is not magic. It is not complicated. But it is designed in a specific way that matches how real people actually behave, not how financial textbooks say they should behave. These 10 reasons explain the difference.

You have tried willpower. Maybe it is time to try a system.

The Total Money Makeover has helped over 5 million people build a budget plan that actually sticks. With more than 22,000 reviews and a 4.7-star rating on Amazon, it is one of the most tested personal finance books in print.

Amazon Check Today's Price on Amazon →It Starts with a Single Small Win

Baby Step 1 is saving $1,000 as a starter emergency fund. That is it. Not $10,000. Not six months of expenses. Just $1,000. For someone who has never saved a meaningful amount, hitting that number in four to six weeks changes the way they feel about money. Ramsey understands that momentum is everything early on. The book explains why this specific number was chosen and why trying to do more before doing this first usually leads to quitting.

The Debt Snowball Beats the Math-Optimal Method

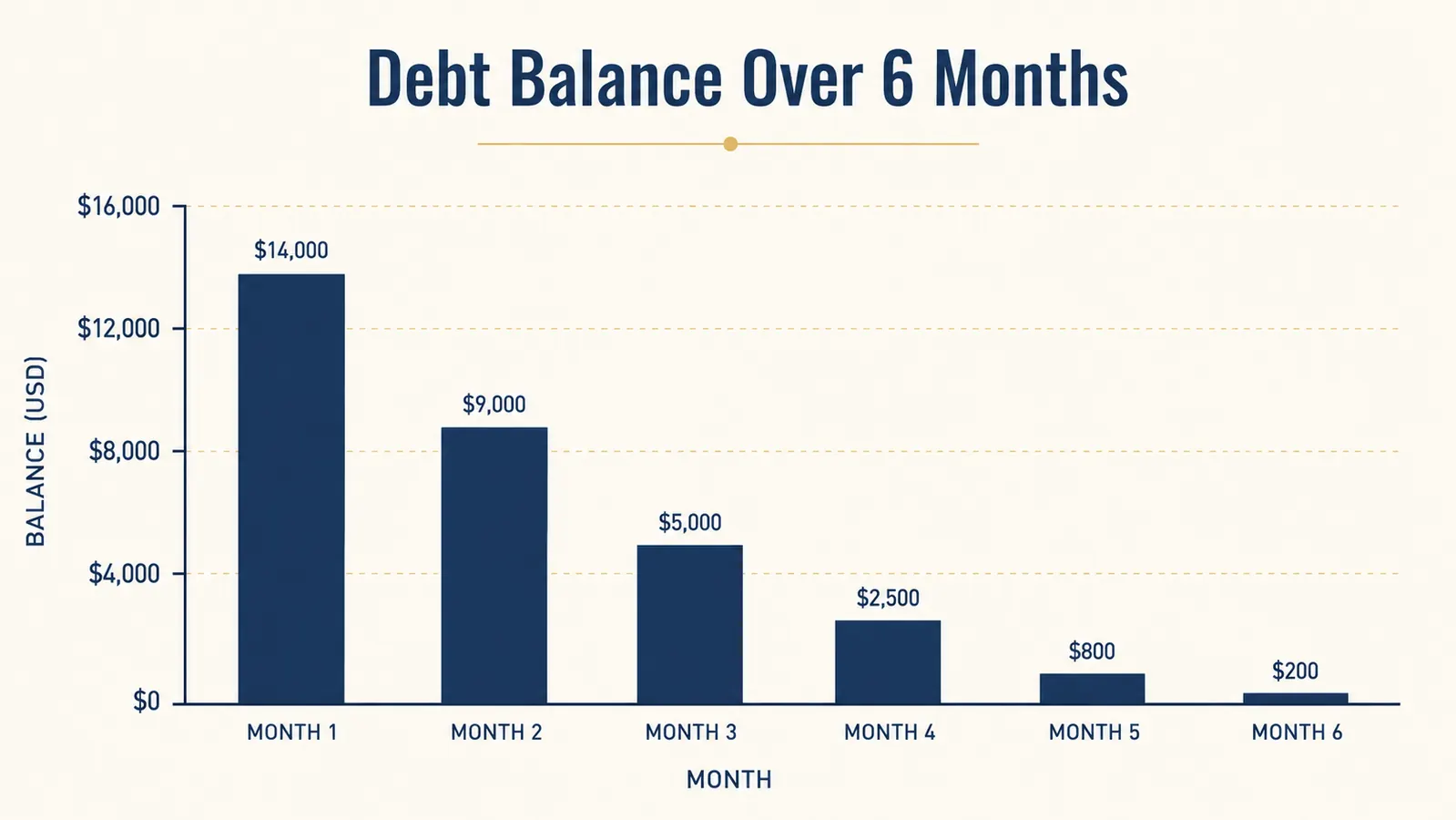

Financial advisors will tell you to pay off your highest-interest debt first. That is technically correct. But most people do not stay on a plan that takes 18 months to feel like it is working. The debt snowball pays off your smallest balance first, regardless of interest rate. The win comes faster. You cancel one debt completely, then roll that payment into the next one. Ramsey lays this out in detail in the book, along with the research showing why behavior beats math when it comes to debt payoff.

Every Dollar Gets a Job Before the Month Starts

Zero-based budgeting means your income minus your planned expenses equals zero. Not because you spend everything, but because every dollar is assigned before it hits your account. Savings and investments are line items, not whatever is left over at the end of the month. Ramsey walks through how to build this kind of budget from scratch, and why people who "try to be careful" with money still lose track without a written plan.

It Treats Money Problems as Behavior Problems

Most budgeting books are about math. Ramsey's book is about choices. He is blunt: the reason most people are in debt is not bad luck, it is habits and patterns that quietly drain income every month. That directness is not comfortable, but it is useful. The book does not let you blame your income for your situation before it asks you to look at what you are actually spending. For people who are ready to be honest with themselves, that reframe is worth the whole book.

The Steps Are Sequential, Not Simultaneous

One of the most paralyzing things about personal finance advice is being told to do six things at once. Pay off debt, build savings, invest 15%, save for college, pay extra on the mortgage. The Baby Steps removes that pressure by telling you exactly which one to focus on right now, and to ignore the others until you get there. That singular focus is why people who follow the plan consistently outperform people who try to optimize everything at the same time.

It Kills the Credit Card Trap Without Lecturing You to Death

Ramsey is not subtle about credit cards: he thinks you should cut them up. His reasoning, explained over several chapters, is that the rewards and cash back people earn rarely offset the extra spending that comes with using credit. He backs this up with consumer behavior research. You can disagree with him, but the book makes its case clearly. For someone who is $8,000 deep in credit card debt and still swiping, the argument lands.

The plan works not because it is clever, but because it is clear. When you know exactly what to do next, you stop stalling.

It Has a Built-In Emergency Cushion Before the Big Push

After you pay off all non-mortgage debt in Baby Step 2, Baby Step 3 is building a full three-to-six-month emergency fund. Most people skip this because it feels like it is slowing down their progress. But this cushion is what keeps people from going back into debt when the car breaks down or the HVAC goes out. The book explains how to size this fund based on your specific situation and why this order matters more than it seems.

The Investment Steps Are Specific, Not Vague

Baby Step 4 is investing 15 percent of household income into retirement. Ramsey does not just say "invest for the future." He tells you what accounts to use first (employer match, then Roth IRA, then back to the 401k), what to look for in mutual funds, and how to think about long-term returns. For someone who has never opened a brokerage account, having that level of specificity in writing is a huge help. The book does not require a financial advisor to understand.

It Works Whether You Are Single or a Couple

The book addresses both solo budgeters and couples, and it handles the couple dynamic honestly. Money fights are common in relationships, and Ramsey dedicates real space to getting on the same page with a partner before starting. He calls it the "budget committee meeting" and gives couples a framework for talking about money without it becoming a fight. I have seen this alone save people a lot of friction in the first month of trying to follow the plan together.

Over 5 Million Copies Sold Is a Real Signal

Books about personal finance come and go. This one has been in continuous print since 2003 and has sold over 5 million copies. It has more than 22,000 reviews on Amazon with a 4.7-star average. That is not a fluke and it is not just marketing. It means enough ordinary people read it, tried it, and saw enough results to come back and write about it. For someone who is skeptical of finance advice, that track record is worth something. You can read my longer breakdown in the <a href="total-money-makeover-review-long-term">Total Money Makeover long-term review</a>.

What I Would Skip

The book is not perfect for every situation. If you have a very high income and are already debt-free, the early chapters will feel basic. Ramsey also has strong opinions about investing only in actively managed mutual funds, which is a point where he parts ways with most low-cost investing advocates. And his stance on credit cards is not workable for everyone, especially people who use a single card responsibly for travel benefits and pay it off monthly. These are real tradeoffs worth knowing before you buy. If you want to pair this with a physical budgeting system, the SKYDUE Budget Binder works well alongside the zero-based budgeting approach Ramsey teaches.

If you are tired of financial advice that does not stick, this is the clearest starting point I know.

The Total Money Makeover walks you through exactly what to do, in what order, and why. It is the kind of book you read once and keep coming back to. More than 22,000 Amazon reviewers agree it is worth the read.

Amazon Check Today's Price on Amazon →