I used to think the tax code was something only accountants understood. Every spring I would hand my W-2 to a preparer, sign where they told me to sign, and hope the refund was decent. It took me three years of doing exactly that before a friend asked me a simple question: did I know about the deduction for my work-from-home space? I did not. I had been leaving money on the table every single year.

Most people in the same position are not being lazy. They just do not know what they are allowed to claim. The IRS does not send you a reminder list. Your tax software is not going to ask fifteen follow-up questions about every corner of your life. That is why a reference like the 475 Tax Deductions for Businesses and Self-Employed Individuals by Bernard B. Kamoroff exists. It is an A-to-Z guide to write-offs that many filers never think to look for. The deductions below are all drawn from that kind of detailed research. A few may apply to you right now. Others depend on your specific situation. Always confirm eligibility with a tax professional or IRS guidance before you claim anything, because the rules have nuances and individual circumstances vary.

Stop leaving deductions on the table every April.

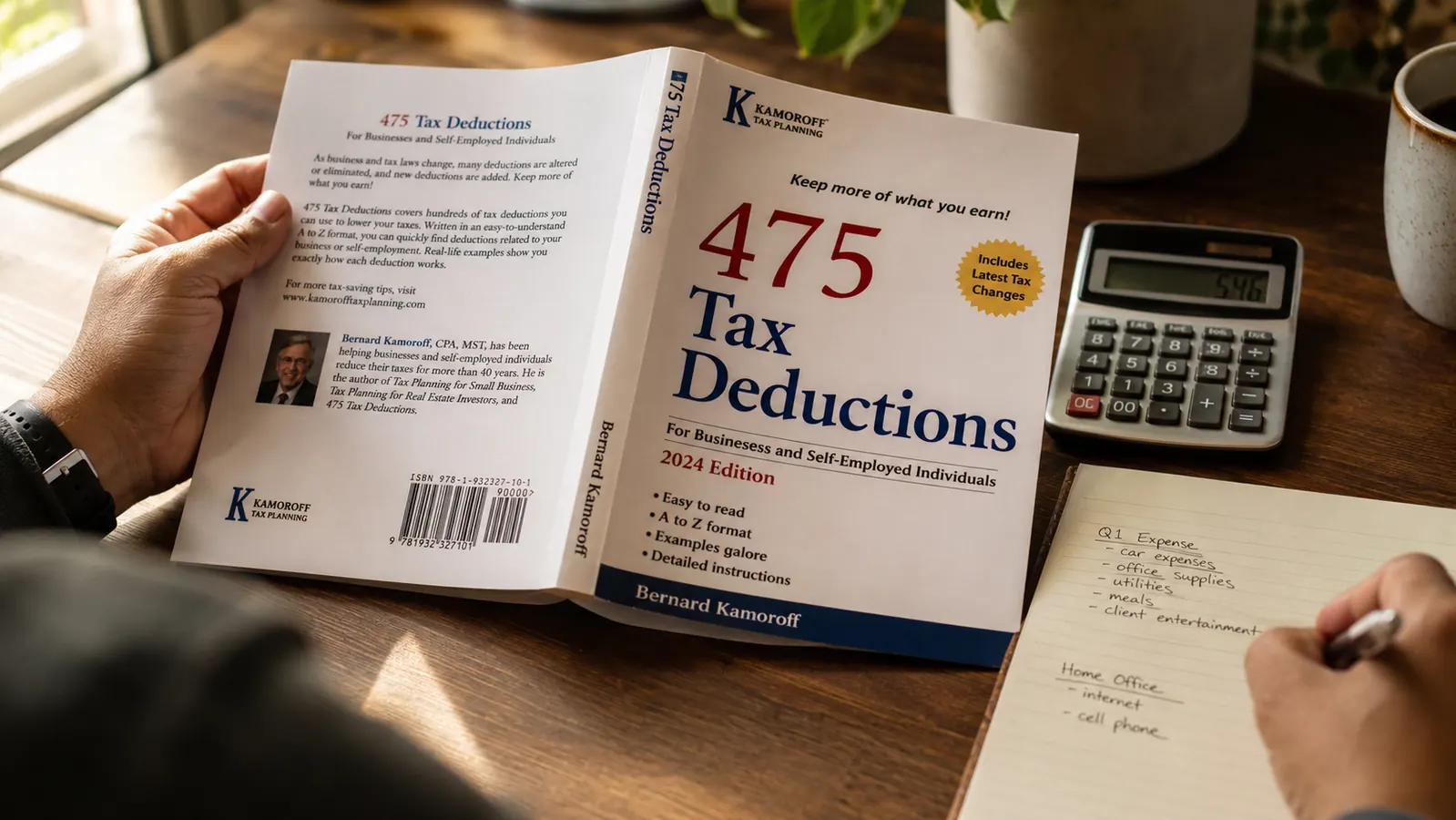

The 475 Tax Deductions book by Bernard B. Kamoroff is the reference guide that spells out write-offs most filers never look for. Over 1,300 buyers have rated it 4.7 out of 5 stars on Amazon. Worth a look before your next filing.

Amazon Check Today's Price on Amazon →Home Office Deduction

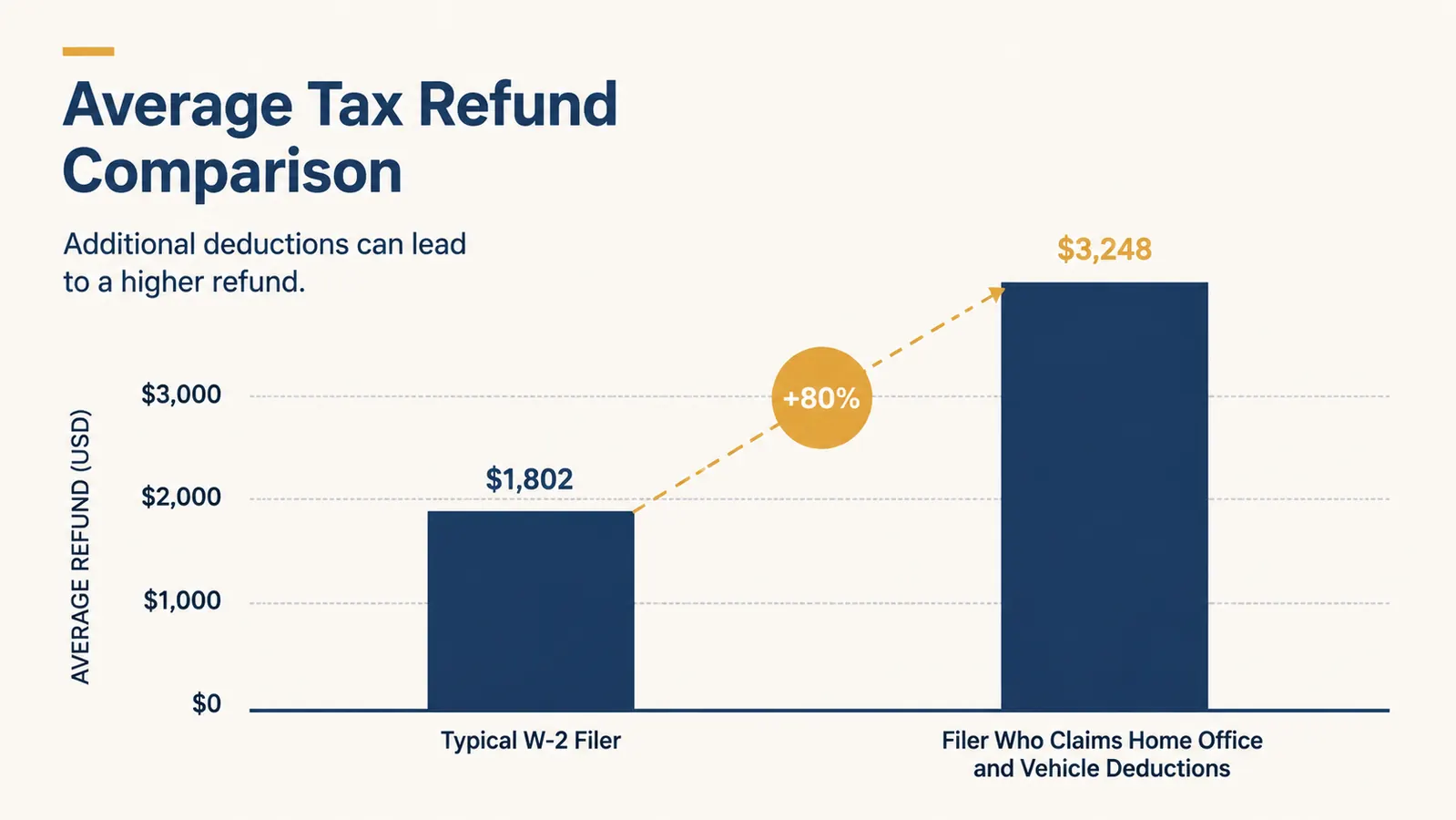

If you use a dedicated portion of your home regularly and exclusively for work, you may be able to deduct a share of your rent or mortgage interest, utilities, and insurance. The IRS offers a simplified method (a flat rate per square foot) that takes some of the math out of it. This deduction is not limited to full-time freelancers. If you have a side gig or run any kind of small business, the space you use for it counts. The 475 Tax Deductions book has a full entry on home office rules, including the exclusive-use test that trips up most filers.

Vehicle Mileage for Business Use

Driving for work is deductible, but most people only think of this if they are a full-time contractor or courier. If you drive to client meetings, job sites, supply stores, or anywhere related to a side business, those miles count. The IRS sets a standard mileage rate each year that you can use in place of tracking actual expenses. The catch is documentation: you need a log of dates, destinations, and purpose. Kamoroff covers the mileage deduction in clear detail, including what records you need to survive an audit.

Self-Employment Health Insurance Premiums

If you are self-employed and pay for your own health insurance, you may be able to deduct 100 percent of those premiums for yourself and your family, even if you do not itemize. This is one of the most valuable deductions for gig workers and small business owners, and one of the most commonly skipped because people assume it only applies to larger businesses. It has income limits and other conditions, so check with a tax professional, but the 475 Tax Deductions guide spells out exactly when and how it applies.

Student Loan Interest

You can deduct up to $2,500 in student loan interest per year, and you do not have to itemize to take it. This deduction phases out at higher income levels, but for most working people paying off loans, it is available and easy to miss because the line on the tax form is easy to overlook. Your loan servicer should send you a Form 1098-E showing how much interest you paid. If you did not get one, log into your servicer account and pull it manually before you file.

Retirement Contributions to a Traditional IRA

Contributions to a traditional IRA can be deductible depending on your income and whether you or your spouse have access to a workplace retirement plan. If you do not have a 401k through your job and you put money into a traditional IRA, you may be able to deduct the full contribution. For many people in that situation, this is one of the most impactful deductions available because it reduces taxable income dollar for dollar, up to the annual contribution limit. Kamoroff's book explains how IRA deductibility phases in and out based on modified adjusted gross income.

The IRS does not send you a list of what you qualify for. You have to know what to ask.

Business-Related Phone and Internet Costs

If you use your phone or home internet connection partly for work or a side business, the business-use percentage of those bills may be deductible. You cannot deduct the whole thing if it is a personal phone you also use for personal calls, but you can estimate the business-use percentage and deduct that share. Most people either skip this entirely or do not realize the deduction extends to internet service, not just the phone itself. The 475 Tax Deductions guide includes a section on communication expenses and how to estimate the business-use portion reasonably.

Professional Development and Education Expenses

Money you spend to improve skills required in your current job can be deductible. This includes courses, books, subscriptions, and professional certifications that relate directly to your work. It does not cover education for a new career, but if you are deepening expertise in what you already do, there is a good argument for the deduction. The line between deductible and non-deductible education can be narrow, so it is worth reading how the IRS draws it. Kamoroff addresses this in the education section of his guide with specific examples of what qualifies and what does not.

Charitable Contributions (Cash and Non-Cash)

If you itemize deductions, cash and non-cash charitable contributions to qualifying organizations are deductible. Most people remember to deduct cash donations but forget about the clothing, furniture, and household goods they drop off at Goodwill or a local charity. Non-cash contributions require a receipt from the organization and a reasonable valuation of what you donated. For donations over certain dollar amounts, you need a written acknowledgment. The IRS has specific rules about how to value used goods, and Kamoroff's book covers both cash and non-cash charitable giving in detail.

Earned Income Tax Credit (Often Unclaimed)

Technically a credit rather than a deduction, but it belongs on this list because it is one of the most valuable tax benefits for working people at lower to moderate income levels, and the IRS estimates that about 20 percent of eligible filers do not claim it. If your income falls within the qualifying range and you have earned income from work, the EITC can reduce your tax bill significantly or even result in a refund larger than what you paid in. Eligibility depends on income, filing status, and number of dependents. The IRS has a free eligibility tool at irs.gov, and Kamoroff covers it in the context of tax planning for self-employed filers.

State and Local Taxes Paid (SALT) Up to the Cap

If you itemize, you can deduct up to $10,000 in state and local taxes, including state income tax or sales tax (your choice), plus property taxes. The $10,000 cap has been in place since 2018 and is a firm ceiling, but many filers who itemize do not add up all the components carefully and end up claiming less than the cap allows. Property tax is the one people most often forget to tally fully, especially if part of it is paid through a mortgage escrow account. Your lender should send a Form 1098 that includes the property taxes they paid on your behalf during the year.

What I Would Skip

Not every deduction you read about online applies to regular W-2 employees who do not have a side business or a home office. Some write-offs circulate on social media that are taken out of context, misapplied, or flat-out wrong. I have seen people try to deduct commuting costs (the IRS does not allow it for most workers), personal meals (not the same as a business meal), and gym memberships without any legitimate business connection. If a deduction sounds surprising and nobody official has confirmed it, look it up on irs.gov or ask a CPA before you claim it. A deduction that triggers an audit and gets disallowed costs you more than it saved.

A reference book you read once at the kitchen table can pay for itself a hundred times over at tax time.

Want the full list of deductions you might qualify for?

The 475 Tax Deductions for Businesses and Self-Employed Individuals by Bernard B. Kamoroff is the kind of reference that pays for itself the first time you find a deduction you did not know you had. Rated 4.7 stars by over 1,300 buyers on Amazon. Check current availability and pricing below.

Amazon Check Today's Price on Amazon →