When I was 29, I had $47 sitting in a savings account earning almost nothing and a vague sense that I was supposed to be investing. Every time I tried to learn how, I landed on an article full of terms like 'expense ratio,' 'asset allocation,' and 'tax-loss harvesting,' and I closed the tab. I thought investing was something people did after they already had money figured out. Turns out I had it backward. Index fund investing is actually one of the simplest things you can do with money, once someone explains it in plain terms.

This guide is that plain-terms explanation. It is not investment advice, and nothing here guarantees any particular return. What it does is walk you through the exact sequence of steps a beginner needs to take to open an account, choose a fund, put in a first dollar, and set up a system that keeps going without you having to think about it every week. The best book I have found for backing up the strategy behind all of this is John Bogle's 'The Little Book of Common Sense Investing,' a slim, readable volume that makes the case for low-cost index funds in language anyone can follow.

Want the book that explains why this strategy works before you put a dollar in?

John Bogle's 'The Little Book of Common Sense Investing' has over 11,000 reviews on Amazon and is consistently recommended as the single best starting point for beginner investors. It is short, it is plain-spoken, and it will give you the confidence to follow through on every step below.

Amazon Check Today's Price on Amazon →Step 1: Open a Brokerage Account or Roth IRA Before You Do Anything Else

The first real decision is where to hold your investments, and the good news is that most beginners have a straightforward choice. If you earn income and fall within the income limits, a Roth IRA is usually the best starting account for someone new to investing. You contribute money you have already paid taxes on, it grows tax-free, and you can withdraw the earnings in retirement without owing a penny more in taxes. As of 2024, you can contribute up to $7,000 per year if you are under 50. That works out to about $583 a month, or $135 a week, but you can start with far less.

If you already have a 401(k) through your job that offers a low-cost index fund option and your employer matches contributions, fund that first up to the match before opening anything else. A 100% match on the first 3% of your salary is a guaranteed 100% return on those dollars, and nothing in the market competes with that. Once you have captured the full employer match, a Roth IRA is the next stop. Fidelity, Vanguard, and Charles Schwab are the three most commonly recommended brokerages for beginners: no account minimums, no commissions on trades, and they all offer their own index funds with very low costs. You can have an account open in about 15 minutes online.

If a Roth IRA is not an option for you right now (maybe your income is above the phase-out limit, or you already max it out), a regular taxable brokerage account at any of those same three platforms works fine. The tax treatment is different, but the fund choices are exactly the same. Do not let this detail stop you from starting. Open an account today, even if it sits empty for a week while you figure out the next step.

Step 2: Pick a Low-Cost Total Market Index Fund and Ignore Everything Else

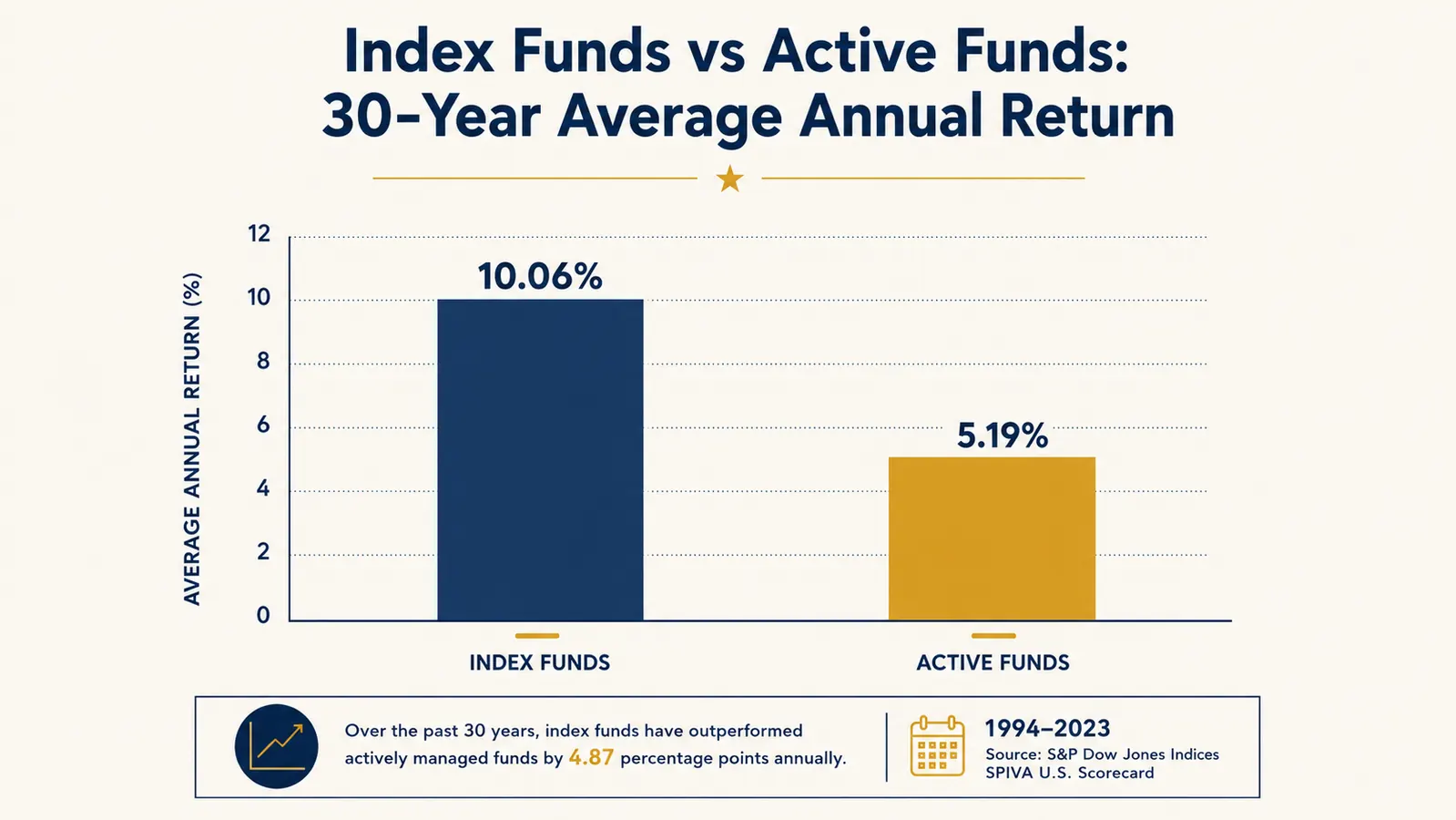

Once your account is open, you need to choose what to actually buy. Here is where most beginners get paralyzed. There are thousands of funds available, and financial media makes it sound like the right choice requires years of expertise. It does not. The core argument of Bogle's 'Little Book of Common Sense Investing' is that a simple, low-cost index fund tracking the entire US stock market gives most investors better results over time than complicated fund-picking strategies, because it keeps costs low and captures whatever the market earns rather than trying to beat it.

At Fidelity, look for FSKAX (Fidelity Total Market Index Fund) or FZROX (Fidelity ZERO Total Market Index Fund, which has a 0% expense ratio). At Vanguard, the equivalent is VTSAX or the ETF version VTI. At Schwab, it is SWTSX. These funds each hold a small slice of hundreds or thousands of US companies. When you own one of them, you own a piece of the entire economy, not a bet on any single company. The expense ratio on all of these is somewhere between 0.00% and 0.04% annually, which means on a $10,000 balance you pay between $0 and $4 per year in fees. That matters enormously over decades.

If your brokerage account is a 401(k) through your employer, you may not see these exact fund names. Look for the fund with 'total market' or 'S&P 500' in the name and the lowest expense ratio on the list. Avoid target-date funds for now if they have higher fees than the plain index fund options. The goal is the simplest, cheapest option that tracks a broad market index. One fund is enough to get started.

Step 3: Automate Your Contributions So You Never Have to Remember

The single biggest edge regular investors have over people who try to time the market is consistency. Not skill. Not special knowledge. Just showing up with the same dollar amount every month, whether the market is up or down. This is called dollar-cost averaging, and it is the mechanism behind most long-term investing success stories. The practical way to do it is to set up an automatic contribution from your checking account to your brokerage account on the same day every month, ideally right after you get paid.

At Fidelity and Schwab, you can set this up in minutes under the account settings or transfer section. At Vanguard, you do it through the automatic investment option. Pick a number that is realistic, not aspirational. If $50 a month is all you can manage right now, that is $600 a year going into an index fund instead of a savings account earning 0.4%. It is real money doing real work. The amount matters less than the habit. You can increase it when your income goes up.

One thing worth setting up at the same time: automatic reinvestment of dividends. Most index funds pay small quarterly dividends, and if you turn on automatic reinvestment, those dividends buy fractional shares of the same fund without you doing anything. Over time, those reinvested dividends can represent a meaningful portion of your total return. Every major brokerage offers this as a checkbox in the account settings. Turn it on once and forget about it.

The goal is not to beat the market. The goal is to not lose to it by paying too much in fees or selling at the wrong time. A boring index fund bought consistently is how most regular people actually build wealth.

Step 4: Ignore the Financial News and Stop Checking Your Balance Every Day

This is the hardest step, and I say that from experience. After I invested my first $200, I checked my account every morning for three weeks. When it dropped 4% in one day, I felt sick to my stomach. When it recovered two weeks later, I felt like a genius. Both of those emotional reactions were noise. Neither told me anything useful about whether I should keep investing or change anything. Bogle spends a significant portion of the 'Little Book' on this point, and it is one of the reasons the book is worth reading even if you already understand the basic mechanics of index funds.

The stock market will drop. It has dropped by 20% or more multiple times in the last 30 years and recovered every time. The investors who came out ahead were almost always the ones who kept contributing through those drops rather than selling. When you sell during a downturn, you lock in the loss. When you stay put and keep buying, you are buying shares at a lower price that will be worth more later if the market recovers, which historically it has. None of this is guaranteed. But panic-selling during a correction has a 100% track record of being the wrong move for long-term investors.

A practical rule: check your investment balance once a month at most, and only to confirm your automatic contribution went through. If the balance is lower than last month because the market dropped, do nothing. If it is higher because the market went up, also do nothing. The only action worth taking is increasing your contribution when you can afford to.

Step 5: Rebalance Once a Year and Adjust as Life Changes

If you are investing in a single total market index fund, rebalancing is mostly a non-issue for the first several years. The fund itself is already diversified across the whole market. But as your balance grows and you possibly add other funds (say, an international index fund for diversification or a bond fund as you get closer to retirement), you will want to check once a year that your mix is still what you intended. For example, if you wanted 90% stocks and 10% bonds but stocks went up a lot, your portfolio might now be 96% stocks. Rebalancing means selling a little of what grew and buying a little of what did not to get back to your target.

For most beginners, a simple annual check around tax time is enough. Pick a date you will remember, look at what you own and what percentage each piece represents, and decide if anything needs adjusting. Most brokerages let you do this in a few clicks. If you are using a Roth IRA, rebalancing inside the account does not trigger a taxable event, which makes it painless. In a taxable account, you will want to think about whether selling a fund that gained value will create a tax bill.

The bigger life changes to watch for: a significant income increase (great time to raise your contribution), approaching retirement (time to gradually shift toward less volatile assets), or a major expense coming up (make sure your emergency fund is separate from your investment account so you never have to sell investments to cover a car repair). Your investment account is not your emergency fund. Keep at least three months of expenses in a plain savings account before you invest a single dollar.

What Else Helps

The steps above are enough to get started, but the hardest part of investing is not the mechanics. It is staying confident in a boring strategy when everything around you is either panicking or chasing the latest hot stock. That is why reading Bogle's 'Little Book of Common Sense Investing' is worth the two or three hours it takes. It explains, clearly and without condescension, why the evidence points so strongly toward low-cost index funds for regular investors. Once you understand why the strategy works, you are much less likely to abandon it when things get bumpy.

The book has more than 11,000 reviews on Amazon with a 4.7-star average, which tells you something about how consistently useful people find it. It is not a thick textbook. You can read it in a weekend. And unlike a lot of financial books, it does not try to sell you on anything complicated. Bogle's whole point is that simple, cheap, and consistent beats clever and expensive almost every time. That is a message this audience, people who are doing this on their own without a financial advisor, needs to hear and believe.

A few other things that help: connecting with a fee-only financial advisor (not a commission-based one) for a one-time session if you have a specific situation like a windfall or a big tax question. Reading our longer review at What Changed After I Read The Little Book of Common Sense Investing and Invested if you want more detail on the book itself before buying it. And checking out 10 Reasons Index Funds Beat Stock Picking for Regular People if you are still on the fence about whether this approach is really better than trying to pick individual stocks.

Ready to understand the 'why' before you invest your first dollar?

The Little Book of Common Sense Investing by John Bogle is the clearest, most readable explanation of why index fund investing works, written by the man who invented the index fund. Over 11,000 Amazon buyers have found it worth their time. Check the current price and pick it up before your next contribution date.

Amazon Check Today's Price on Amazon →