Two years ago I had $400 sitting in a savings account earning almost nothing, a vague sense that I should be investing, and absolutely no idea where to start. A coworker mentioned The Little Book of Common Sense Investing by John C. Bogle. She said it was short, plain-spoken, and had changed the way she thought about her 401k. I checked the current price on Amazon, bought it, and read it in a weekend. What I found inside was not a get-rich plan. It was something more useful: a clear, honest explanation of why most people lose money trying to beat the market and a dead-simple alternative that costs almost nothing to follow.

I want to be honest with you the way that coworker was honest with me. This is not a book that will make you feel excited or inspired the way some financial titles do. Bogle's writing is calm and methodical. But two years into applying his core idea, I have watched my small, consistent index fund contributions grow in a way that nothing else in my financial life has. That is what I want to walk you through.

The Quick Verdict

The clearest, most honest case for low-cost index fund investing ever put into a single short book. A little dry in the middle chapters, but the core argument is airtight and the advice is immediately actionable even for someone starting from zero.

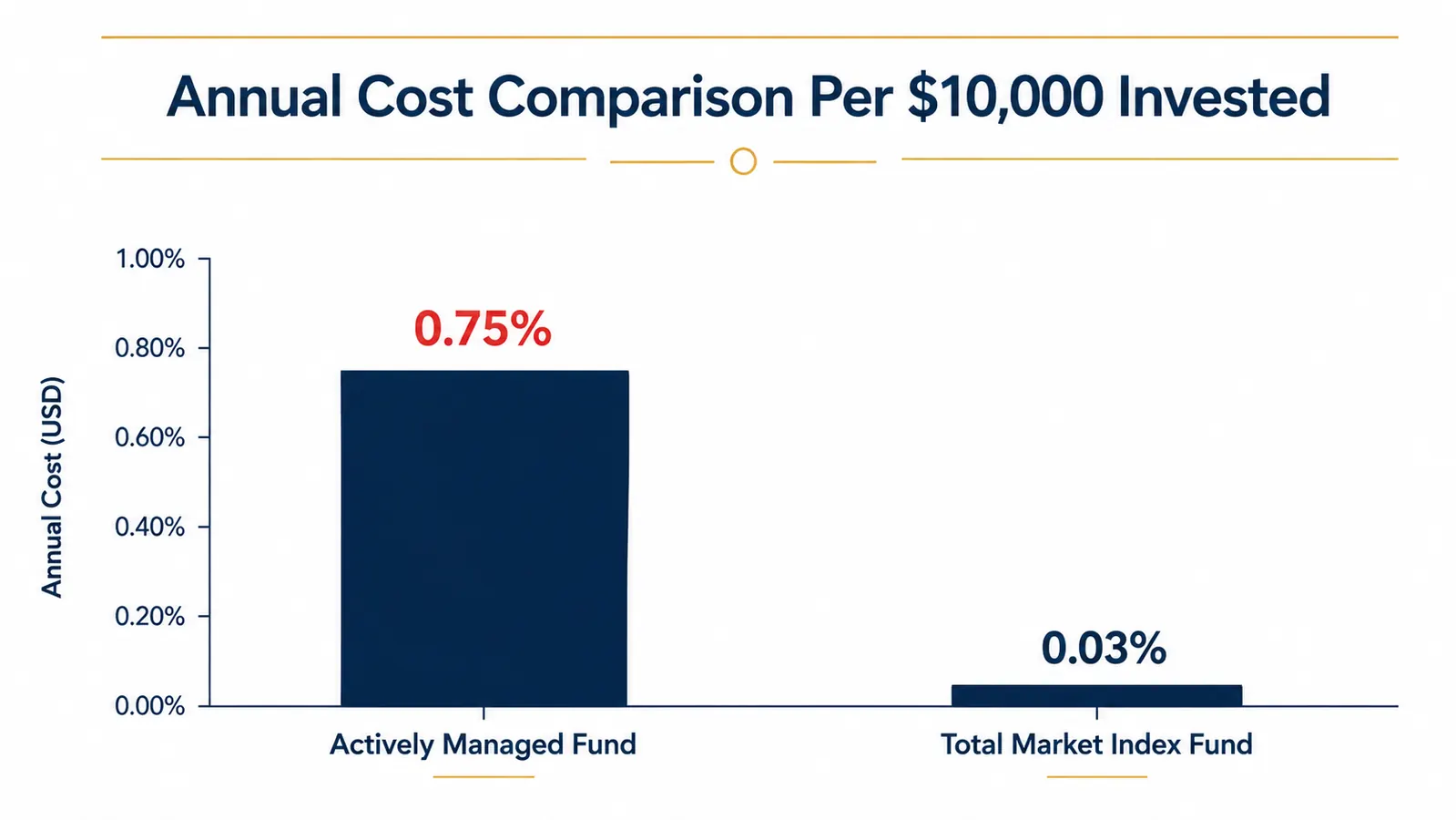

Amazon Check Today's Price →Still paying 0.75% in fund fees when 0.03% is available? Bogle explains exactly why that gap costs you more than you think.

The Little Book of Common Sense Investing has over 11,000 ratings on Amazon for a reason. It is a short read with a lasting payoff.

Amazon Check Today's Price on Amazon →How I Read It and What I Did Afterward

I sat down with the book on a Saturday morning with coffee and a notepad. Bogle does not waste your time. The first chapter lays out the central argument in plain terms: the stock market returns what it returns, and most of the money you lose to active investing comes from the fees and trading costs you pay trying to beat it. Every dollar in fees is a dollar that stops compounding. Over decades, that math is brutal.

By Sunday afternoon I had finished it and written down three action steps. First, I opened a Roth IRA with Fidelity and put my $400 into a total market index fund with a 0.015 percent expense ratio. Second, I set up a $50 automatic contribution on every payday. Third, I wrote on a sticky note: 'Do not touch it. Do not check it every day. Let it compound.' That note is still on my monitor.

Twenty-four months later, my account balance reflects those 48 contributions plus market movement. I am not going to quote a specific dollar return because market conditions vary and past performance tells you nothing reliable about your future results. What I will tell you is that the discipline the book instilled, put money in consistently and stop trying to be clever about it, has been worth far more to me than any stock tip I ever read online.

What Bogle Is Actually Arguing

The book's central claim is straightforward: the average actively managed mutual fund underperforms a simple total market index fund over the long run, primarily because of costs. A fund that charges 1 percent per year in fees needs to outperform the market by more than 1 percent every year just to break even with the index. Most do not. Bogle backs this up with decades of fund performance data, and the argument is hard to argue with once you see the numbers laid out clearly.

He is not saying the market never goes down. He is not saying index funds are a way to get rich fast. He is making a quieter point: over long periods, getting your fair share of the market's overall growth while paying rock-bottom fees is a better outcome than most professional fund managers deliver for their clients. That is not a thrilling story. It is a true one. If you want to see exactly why this holds up across dozens of real-world fund comparisons, our breakdown of 10 reasons index funds outperform stock picking for regular investors goes deeper on the data.

Bogle is not asking you to be clever. He is asking you to be patient and keep your costs low. Those two things together turn out to be more powerful than most people expect.

The updated edition of the book also covers ETFs (exchange-traded funds), which are index funds you can buy like a stock. This is useful because some brokerage accounts make ETFs easier to access than traditional index mutual funds. Bogle's guidance on both is consistent: keep the expense ratio as low as possible, diversify broadly, and resist the urge to trade.

What the Book Does Exceptionally Well

The strongest part of the book is its honesty about the investing industry. Bogle spent his career at Vanguard, which he founded, and he does not pull punches about how the mutual fund industry profits at the expense of investors. He calls fees a 'tyranny of compounding costs.' He is specific about the math. If the market returns 7 percent over the long run and your fund charges 1 percent, you are keeping 6 percent. But because of compounding, that 1 percent fee does not cost you 1 percent. Over 30 years it can cost you somewhere around 20 to 25 percent of your ending balance. Seeing that laid out plainly changed how I looked at every fund I had ever considered.

The book is also remarkably short for its ambition. The 10th anniversary edition runs about 216 pages but reads much shorter because Bogle is not padding. Every chapter has a clear point and he makes it, then moves on. For someone who feels behind on personal finance and overwhelmed by the sheer volume of content out there, that concision is a genuine gift.

A third thing the book does well is make peace with market downturns. Bogle's framing is essentially this: if you are investing money you will not need for 20 or 30 years, then a market drop is not a loss, it is a sale. You are buying more shares at a lower price with each contribution. That mindset shift is not something you can get from watching financial news. It requires understanding why the strategy works, and the book gives you that understanding in a way that sticks.

Where the Book Falls Short

The weakest chapters are in the middle, where Bogle gets technical about historical fund data and regression analysis. If you are a first-time investor who just wants to know what to do, those sections can feel like reading a textbook. I skimmed several of them without losing the thread. You do not need to understand every chart in the book to apply its core lesson.

The book also does not tell you how to start. Bogle explains what index funds are and why they work, but he does not walk you through opening a brokerage account, choosing a specific fund ticker, or setting up automatic contributions. If you have never invested before, you will finish the book convinced and then sit there wondering what the actual first step is. You will need a separate resource for the mechanics. That gap is real and it is worth knowing about before you buy. For context on how this compares to a more beginner-tactical book, see our article on The Little Book of Common Sense Investing versus The Intelligent Investor.

There is also a narrow focus on equities. Bogle's argument is specifically about stock index funds. He covers bond index funds briefly, but the book does not help you think through asset allocation, how much to put in stocks versus bonds, or how your mix should change as you get closer to needing the money. For a true beginner who wants the complete picture, you may find yourself reaching for a second book alongside this one.

What I Liked

- Clear, data-backed case for low-cost index fund investing that holds up under scrutiny

- Short enough to read in a weekend without losing the argument

- Honest about how the fund industry works and who benefits from high fees

- Changes how you think about fees and compounding in a lasting way

- Updated edition addresses ETFs and modern brokerage access

- Bogle writes from lived experience founding and running Vanguard, not from theory

Where It Falls Short

- Middle chapters are dense with historical data and feel like a textbook

- Does not explain how to actually open an account or buy your first fund

- Narrow focus on stock index funds leaves out the broader asset allocation question

- Bond fund and retirement timeline guidance is minimal

- Readers who want a concrete action plan may feel stranded after the last page

How It Holds Up Two Years Later

The market has had good stretches and rough stretches in the two years since I read this book. In the rough stretches I went back to my sticky note. I did not sell. I kept contributing. I have no way to guarantee what my account will look like in 10 or 20 years, and Bogle would not guarantee it either. What I can tell you is that the discipline he teaches is genuinely hard to maintain if you are watching financial news and trying to time things. It is much easier to maintain if you understand why staying the course matters, which is exactly what the book teaches.

One thing I did not expect is how often I come back to the book's ideas when someone at work brings up a hot stock or a new ETF with a clever strategy. The book gave me a clear framework for evaluating any investing claim: what are the costs, and does the evidence show this consistently outperforms after costs over long periods? Almost nothing passes that test except a plain index fund. Having that filter in my head has saved me from at least two decisions I would have regretted.

I have recommended this book to four people in my circle since reading it. Two of them have opened their first investment accounts as a result. One of them is my younger sister, who was 23 at the time and had never invested anything. She started with $25 a paycheck. That is what this book does: it lowers the perceived barrier to starting because it simplifies the decision to something almost anyone can act on.

Who This Is For

This book is for you if you know you should be investing but feel paralyzed by the options, intimidated by the jargon, or suspicious that there has to be a catch somewhere. It is also for you if you already have a 401k but have never looked closely at what funds you are in or what they cost. Bogle gives you the framework to answer both of those problems, and the framework is not complicated. Low cost, broad diversification, long time horizon. That is the whole thing. The book just explains why that is the whole thing, with enough data behind it that you actually believe it.

It is also a good fit if you are someone who has tried to pick individual stocks or follow active fund managers and found the experience frustrating or confusing. Bogle does not shame you for trying. He just shows you why the math works against most active strategies over time and offers a calmer, simpler path forward.

Who Should Skip It

If you are already investing in low-cost index funds and you understand why you are doing it, this book will not teach you much you do not already know. The core argument is powerful, but it is also singular. There is not a lot of range here. If you are looking for guidance on real estate investing, individual stock analysis, retirement income planning in detail, or tax strategy around your investments, you will need a different book. This one does one thing, and it does it well. But it is only one thing.

Also, if you need something that hands you a specific to-do list with fund names and account steps, you may want to pair this with a more hands-on resource. Bogle is making a philosophical and mathematical case. The tactics are yours to figure out. That can feel like an incomplete handoff if you were hoping for a full step-by-step guide. If you want the step-by-step alongside the why, our article on how to start investing in index funds as a beginner walks through the actual account setup after you finish the book.

If you have been telling yourself you will start investing once you understand it better, this is the book that makes that possible.

The Little Book of Common Sense Investing is short, honest, and has over 11,000 readers who found it worth their time. Check today's price on Amazon.

Amazon Check Today's Price on Amazon →