Let me tell you the thing that surprised me most about The Total Money Makeover: I went in expecting to disagree with it. I had heard the criticisms. Too preachy. Too rigid. Credit cards are not the enemy, discipline is. The debt snowball is mathematically inferior to the avalanche. I had read those takes. And then I sat down and actually read the book, all 240-something pages, and came away with a more complicated opinion than either the devoted fans or the loudest critics seem to hold. This review is that opinion.

I should tell you who I am so you can calibrate. My name is Angela, I work in healthcare administration, I make about $54,000 a year in a mid-size Tennessee city, and I came to this book after a coworker mentioned it during a break room conversation about rising grocery bills. I had about $14,200 in debt at the time: a credit card, a personal loan from a family member I had been slow to pay back, and a small balance on a medical bill. I was not in crisis but I was not moving forward either. I picked up the book to see what the fuss was about, and I read it with a highlighter and a notepad, treating it like homework.

The Quick Verdict

A blunt, effective system for people who are stuck on debt and need someone to stop being gentle about it. Works best if you commit fully and borrow the parts that fit your life rather than treating every sentence as law.

Amazon Check Today's Price →Still circling the same debt every month with no real plan? This is where most people finally stop circling.

The Total Money Makeover has over 22,000 verified reviews on Amazon and a 4.7-star average. It is the most consistently recommended starting point in personal finance for a reason. Read it once through before you decide whether to follow it.

Amazon Check Today's Price on Amazon →What Nobody Tells You Before You Read It

The first thing that caught me off guard is how little time the book spends on budgeting techniques compared to how much time it spends on mindset and motivation. I expected a financial workbook. What I got was closer to a financial intervention. Ramsey is not trying to teach you a spreadsheet system. He is trying to change the way you think about money, debt, and what is normal. That framing matters because it explains why some people love the book deeply and others bounce off it completely. If you are resistant to being challenged, the tone will read as preachy. If you are ready to be challenged, the same tone reads as the first honest conversation about money you have ever had.

The second thing nobody tells you is that the baby steps are deliberately simple and that simplicity is not a flaw. Critics sometimes say the plan is too basic, that it ignores tax-advantaged debt, or that it does not account for behavioral economics research that has come out since Ramsey started writing. All of that is arguably true. But the people who benefit most from this book are not people who are analytically paralyzed by complexity. They are people who know they have a problem and do not know where to start. For that person, a clear and specific seven-step sequence is not too simple. It is exactly what they needed.

The third thing: there is a version of this book that is not for you. If you are already a disciplined budgeter who is looking for portfolio optimization advice, you will find the wealth-building sections thin. Ramsey recommends 15% into retirement accounts and mentions mutual funds with a four-fund portfolio strategy, but he does not go deep on how to choose funds, what expense ratios mean, or how to construct a portfolio across tax types. He points you toward a financial advisor, specifically one in his network. That is not a dealbreaker but it is worth knowing.

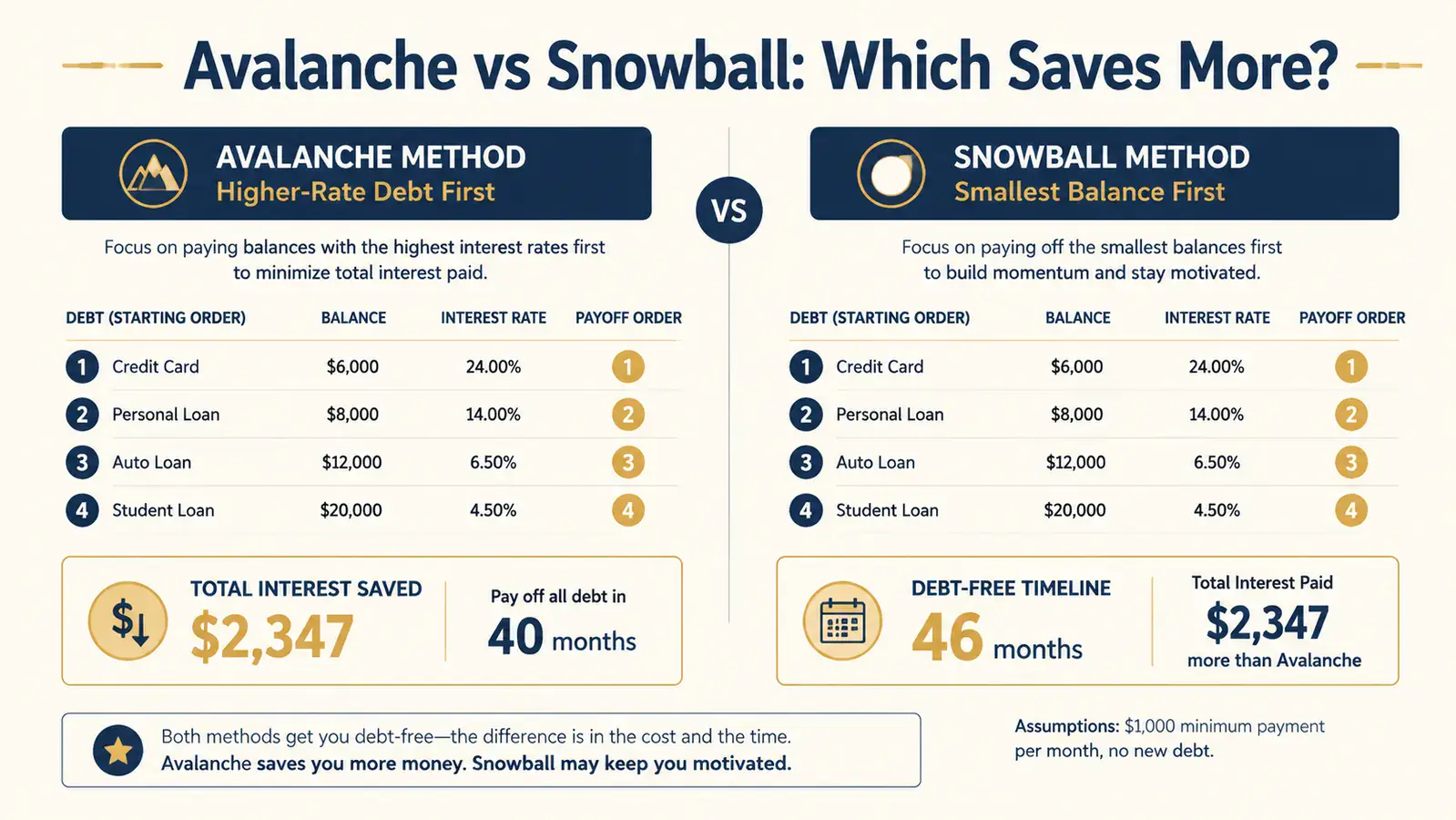

The Snowball Debate: Honest Take

The debt snowball, which tells you to pay off your smallest balance first regardless of interest rate, is the most criticized part of the book. The math critics are right: if you have a $2,000 card at 8% and a $500 card at 22%, the avalanche method (highest rate first) will save you more money in total interest. Nobody disputes that. Ramsey disputes something different. He argues that most people who try the avalanche method fail to complete it because they go months without a win and lose motivation. That is not a math claim, it is a behavioral claim, and there is actually research supporting it.

My own experience: I used the snowball. I paid off my medical bill first, which was the smallest balance at $900. It took about eight weeks. The moment I made the final payment, something clicked in a way I had not felt from any of my budgeting app dashboards. I genuinely believe I would not have stayed the course if I had started with my credit card, which was the highest-rate debt but also the largest balance. That first win bought me the commitment to keep going. For me personally, the snowball was worth the small extra interest cost.

Ramsey does not lose sleep over the avalanche math argument. He is betting that you will never reach month fourteen of a payoff plan if you have not had a single win by month four. Based on my experience, he is probably right.

The Credit Card Question

Ramsey's position on credit cards is the most polarizing thing in the book. He tells you to cut them up, close the accounts, and never use them again. Full stop. His reasoning is that the rewards programs are designed to get you to spend more than you would with cash, that the average person who uses credit cards spends more in total than someone who uses cash, and that the psychological separation between swiping and paying makes overspending easy. He is correct about all of those things as general patterns.

Where I part ways with him is on the absolutism. There are people who pay off their full balance every month and treat credit cards as a payment mechanism rather than a borrowing mechanism. For that person, the rewards and fraud protection are genuine benefits and the risks Ramsey describes do not apply. I kept one credit card after reading the book, used it only for gas and groceries, and paid it in full each month. I did cut up the other two. That felt like a reasonable middle ground. The important thing to understand is that his argument is aimed at the person who cannot keep a zero balance, not necessarily at every person who owns a card. Read the argument for yourself and decide where you fall.

The Parts That Genuinely Helped Me

I want to be clear that this review is not a takedown. The Total Money Makeover changed specific things in my financial life and I am better for having read it. The most valuable chapter for me was the one on the starter emergency fund, which Ramsey calls Baby Step 1. Before reading this book I had no emergency fund at all, because I always told myself I would start one once I paid off more debt. What Ramsey convinced me of is that the emergency fund comes first precisely because without it, any unexpected expense will go straight onto a credit card and restart the debt cycle. He was right. I saved $1,000 into a separate account before I paid an extra dollar on any debt. Three months later my car needed a repair. I paid it from the emergency fund and did not touch my credit card. That one shift was worth the price of admission.

The zero-based budget concept is the other thing I have actually kept. In zero-based budgeting you assign every dollar of your monthly income to a specific category before the month begins, so your income minus your planned spending equals zero. You are not leaving money floating around to be spent on impulse. Every dollar has a name. I had been doing what I now recognize as category budgeting, where you track what you spent versus what you planned, after the fact. Zero-based budgeting is harder upfront but it eliminates the end-of-month surprise. I have used it every month since I read the book.

The chapter on what Ramsey calls the wealth-building steps, which begin once you are out of consumer debt, did something important for me even though I am not there yet. It gave me a reason to keep going. When you are in the middle of a multi-year debt payoff, it is easy to feel like you are just treading water and the finish line is impossibly far off. Ramsey maps out what comes after the debt: retirement investing, college savings, paying off the house, then building and giving generously. That arc made the whole thing feel purposeful rather than just punishing.

What the Book Does Not Cover (And You Will Need Elsewhere)

The income side of the equation gets short shrift. Ramsey repeatedly says to increase your income, get a second job, sell things around the house, be intense. That is true advice but it is not detailed advice. He does not discuss negotiating your salary, switching industries, building skills that increase earning power, or how to think about time investment on side work. If your situation requires more income rather than just tighter spending, you will need a different resource for the specifics. The book is written for someone whose core problem is spending and debt, not for someone whose core problem is earning.

Irregular income is also barely addressed. Ramsey's system assumes a regular monthly paycheck, which you can plan around. If you do gig work, freelance, receive commissions, or have any income variability, the zero-based budget requires modification that the book does not walk you through. You can adapt the framework, but you will be doing that adaptation on your own.

The investing sections, as noted earlier, are introductory. He recommends growth stock mutual funds and mentions the four categories he prefers, but does not compare them to index funds or discuss fee structures in any depth. If you want a thorough grounding in how to actually invest your 15%, the Total Money Makeover will get you started but you should follow it up with something more specific to investing. I have read a comparison of this book against another popular personal finance bestseller if you want a sense of where each one starts and stops: the Total Money Makeover vs The Psychology of Money piece goes into how they complement each other rather than compete.

The Tone: Why It Helps Some People and Irritates Others

Ramsey's voice is not for everyone and I think that is worth naming plainly. He is direct to the point of bluntness. He uses sports analogies and has a southern preacher cadence that runs through the whole book. He has religious references scattered throughout, never dominant but present. He does not hedge. He does not say, well, it depends on your situation. He says here is what you should do and here is why everything else is a mistake. Some people find that energizing. Others find it alienating. I found it somewhere in between: I needed the clarity and I was occasionally annoyed by the certainty. If you are someone who has heard three conflicting money opinions and just wants someone to tell you what to do, Ramsey will feel like a relief. If you prefer a more nuanced, analytical voice, there are better-written books that may land better for you. The results, though, are hard to argue with across 22,000 reviews and over five million copies sold.

What I Liked

- The baby steps are a clear, sequenced plan that removes decision paralysis, you always know what to do next

- The debt snowball works behaviorally even when it does not work optimally on paper

- Zero-based budgeting is a real system that creates accountability before spending, not after

- The starter emergency fund chapter alone prevents most people from falling back into debt mid-payoff

- Written in plain language that does not assume any financial background

- The arc from debt to wealth-building gives a motivating long view, not just a near-term payoff plan

Where It Falls Short

- Income-building advice is brief and not specific enough for someone whose main gap is earning, not spending

- The no-credit-card-ever rule is an absolute where a nuanced position would serve more readers

- Irregular or variable income is barely addressed, making the system harder to apply for gig and freelance workers

- Investing guidance is introductory only, you will need a follow-up resource once you reach Baby Step 4

- The tone is confident to the point of occasional overstatement, which can feel off-putting in complex situations

Who This Is For

This book is for someone who has debt, feels stuck, and has not yet found a plan they will actually follow all the way through. It works best for people who respond to clear rules over flexible frameworks, who want to be told what to do in a direct voice, and who are ready to make some real changes to their spending rather than just read about why they should. It also works well for couples who need to align on money before they can move forward together. The book's straightforward structure gives couples something concrete to discuss and agree on, rather than having vague intentions that fall apart under pressure. It is not the most sophisticated personal finance book available. It is arguably the most actionable one for the person who needs to get started.

Who Should Skip It

Skip this book if you are already debt-free and want investing depth. You will get more from a dedicated investing book at that stage. Skip it if you find prescriptive, confident voices exhausting rather than clarifying. Skip it if your financial situation involves significant complexity like self-employment with quarterly taxes, investment property, or a high income with tax optimization needs. The baby steps assume a relatively straightforward earned-income situation and the plan does not adapt well at the edges. And if you are curious about the mindset side of money rather than the mechanics, something like the approach discussed in the Rich Dad Poor Dad review on this site covers a very different but complementary philosophy worth knowing about.

If debt is the problem and a clear plan is what you are missing, this is the book most people point to when they describe the moment things turned around.

The Total Money Makeover has 22,000 reviews for a reason. It is not a perfect book. But for someone who is ready to stop circling and start a real plan, it delivers. Read it with a highlighter and a notepad, not as a list of commandments but as a framework you adapt to your situation.

Amazon Check Today's Price on Amazon →